Cash accounting shows what’s in your wallet, while accrual accounting shows what you’ve earned and owe, even if the money hasn’t moved yet.

The Two Main Methods of Recording Transactions in Accounting

In accounting, there are two main ways to record transactions: cash accounting and accrual accounting. The difference lies in when income and expenses are recorded.

With cash accounting you only record money when it actually changes hands like when a spaza shop notes sales only when customers pay cash.

Accrual accounting, on the other hand, records income when it is earned and expenses when they are incurred, even if the cash hasn’t moved yet. This gives a more accurate picture of profit and obligations.

Most companies use accrual accounting, but in South Africa, only sole proprietors and partnerships with a turnover below R2.5 million are allowed to use cash accounting.

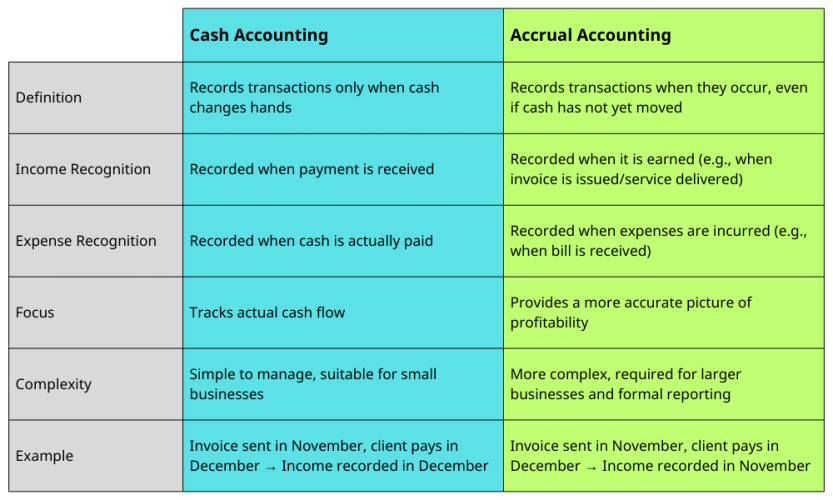

Cash Accounting vs Accrual Accounting

Cash Accounting records income only when cash is received and records expenses only when cash is paid. This method tracks the actual flow of money in and out of the business, making it simple to manage and easy for small businesses to understand. It is commonly used by sole proprietors and informal traders. However, because it ignores money owed or bills not yet paid, it may not reflect the true profitability of the business.

Accrual Accounting records income when it is earned, even if payment has not yet been received, and records expenses when they are incurred, even if they have not yet been paid. This method matches income and expenses to the correct period, giving a more accurate picture of financial health. It is required for larger businesses and formal reporting, and it supports better forecasting and planning.

In short, cash accounting shows what money is physically available, while accrual accounting shows the bigger picture of profitability and obligations.

Summary